That is better: A great HELOC otherwise a home collateral mortgage?

Was HELOC prices repaired?

Like credit cards, HELOCs normally have adjustable rates, meaning the pace you initially located can get increase otherwise slip through the your draw and you can payment episodes. However, particular loan providers americash loans Fairview have begun giving choices to transfer most of the otherwise region of the variable-speed HELOC with the a fixed-rates HELOC, often to own an extra commission.

Is actually a beneficial HELOC tax deductible?

Attract reduced for the good HELOC try tax-deductible so long as its regularly purchase, build otherwise considerably help the taxpayer’s family one secures the borrowed funds, according to the Internal revenue service. Attract is actually capped on $750,one hundred thousand for the lenders (mutual mortgage and you will HELOC or household equity mortgage). So if you had good $600,100000 financial and you may a beneficial $3 hundred,100000 HELOC having renovations towards the a home worth $1.2 mil, you might simply deduct the interest towards earliest $750,000 of your $900,100 you borrowed.

By using a HELOC your purpose apart from home improvement (such as for example undertaking a business otherwise merging higher-notice loans), you cannot deduct focus beneath the tax law.

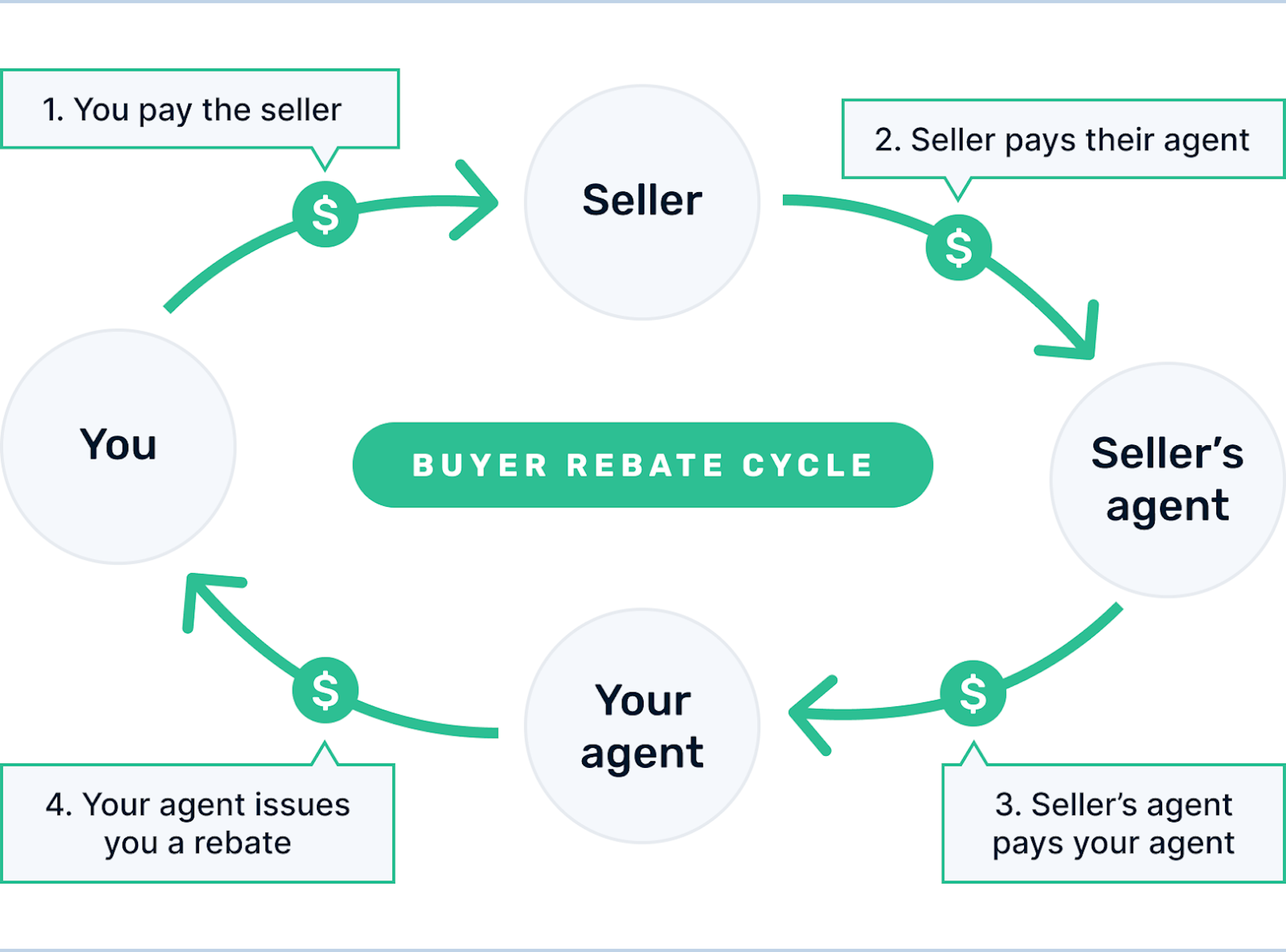

A HELOC usually has an extended installment months and you will allows you when planning on taking just the currency need, as it’s needed, therefore it is ideal for individuals with ongoing expenditures otherwise those people exactly who love to pay back personal debt on their rate.

A property collateral financing, additionally, also offers a lot more predictability with respect to monthly obligations, since the you get a giant amount of cash initial and shell out it back into monthly payments with a fixed interest. Household guarantee money are often good for those who you would like a beneficial lump sum payment instantly and want a predictable payment per month.

Will a good HELOC hurt my personal credit rating?

Because HELOCs is revolving credit lines, they are able to effect, plus damage, your borrowing. Once you pertain, typically the bank will run an arduous query to evaluate your own creditworthiness, and will have a tiny influence on your credit score. While you are a challenging inquiry might cause your credit rating to drop a few facts, just be capable get well men and women activities if one makes prompt payments on your own HELOC harmony.

That being said, a good HELOC will even more significantly damage your credit rating for individuals who are not able to generate towards-go out payments or you skip repayments altogether. In addition, you run the risk out-of shedding your home, while the a HELOC spends it as collateral.

Try HELOC interest levels higher than home collateral otherwise personal loans?

HELOC rates is less than interest rates getting household collateral financing and private fund. But not, HELOC cost plus is varying, which means cost you’ll boost according to conclusion on the Government Reserve.

Would you pay back a great HELOC very early?

Sure, you can pay off an excellent HELOC very early without getting penalized. Should you want to prepay, try to do it when you look at the interest-only several months you prevent paying alot more into the installment big date body type.

Things to watch out for: Third Federal charges a beneficial $65 yearly payment, which is waived into the first 12 months. In addition, discover a minimum monthly payment off $a hundred.

As to the reasons Shape is best family security credit line to have punctual financing: Figure promises an easy on the web software techniques with approval in the four times and you may investment in as little as five business days. Figure might possibly be advisable having borrowers who are in need of punctual bucks.

As to the reasons PenFed Credit Relationship is best household equity collection of credit to possess flexible membership conditions: If you find yourself PenFed possess a track record of providing solution players, you’ll be able to qualify for subscription when you are a member of almost every other discover organizations.

- Affordability: Minimal Apr, intro Annual percentage rate, reduced prices for vehicle-payers and you will fees

- Cash-aside refinance — Whenever you can be eligible for a lower interest than what you’re currently using on your own mortgage, it is possible to re-finance your financial. For folks who refinance to have an expense that’s more than your existing mortgage balance, you could potentially pocket the difference inside the cash.

Good HELOC isnt sensible if you don’t have a constant money or a financial plan to repay the financing. As you make use of family as the equity, if you’re unable to make repayments entirely and on day, your risk losing your home.

Закладки

Comments are closed

Sorry, but you cannot leave a comment for this post.