Tap into their house’s security having financial independency

I’d like a beneficial HELOC, to take cash-out away from my personal house’s guarantee. Can i buy an appraisal, shortly after my lender did an automated appraisal that exhibited a lower well worth than just my house will probably be worth?

I bought my personal domestic cuatro days ago as well as the home based assessment cherished my personal household on $220k. My tax appraisal came in from the $209k. Cost in my own neighborhood has grown somewhat since i have encountered the appraisal. I removed a great HELOC nevertheless the bank’s robo-appraisal simply came back during the $190k. Would it be beneficial to pay $350 for the next in home appraisal, hoping the worth of the home is high? The lending company won’t accept the one currently complete. My personal home loan balance was $175k and i also you need financing to possess $25k.

You will find some separate products within your own matter: the type of assessment a loan provider might require, the fresh new LTV you really need to meet the requirements, and you can whether you should purchase an appraisal up until loan places Snyder now.

Variety of Appraisals

Because you most likely see, the newest taxman’s valuation of your house affects simply how much you have to spend in property fees. When a taxation assessor provides a particular dollars worth on the domestic, it will be the government’s viewpoint of residence’s reasonable-market price. not, the actual dollar testing is not utilized by any mortgage lender, nor can you make use of it to decide a sale rate for your house.

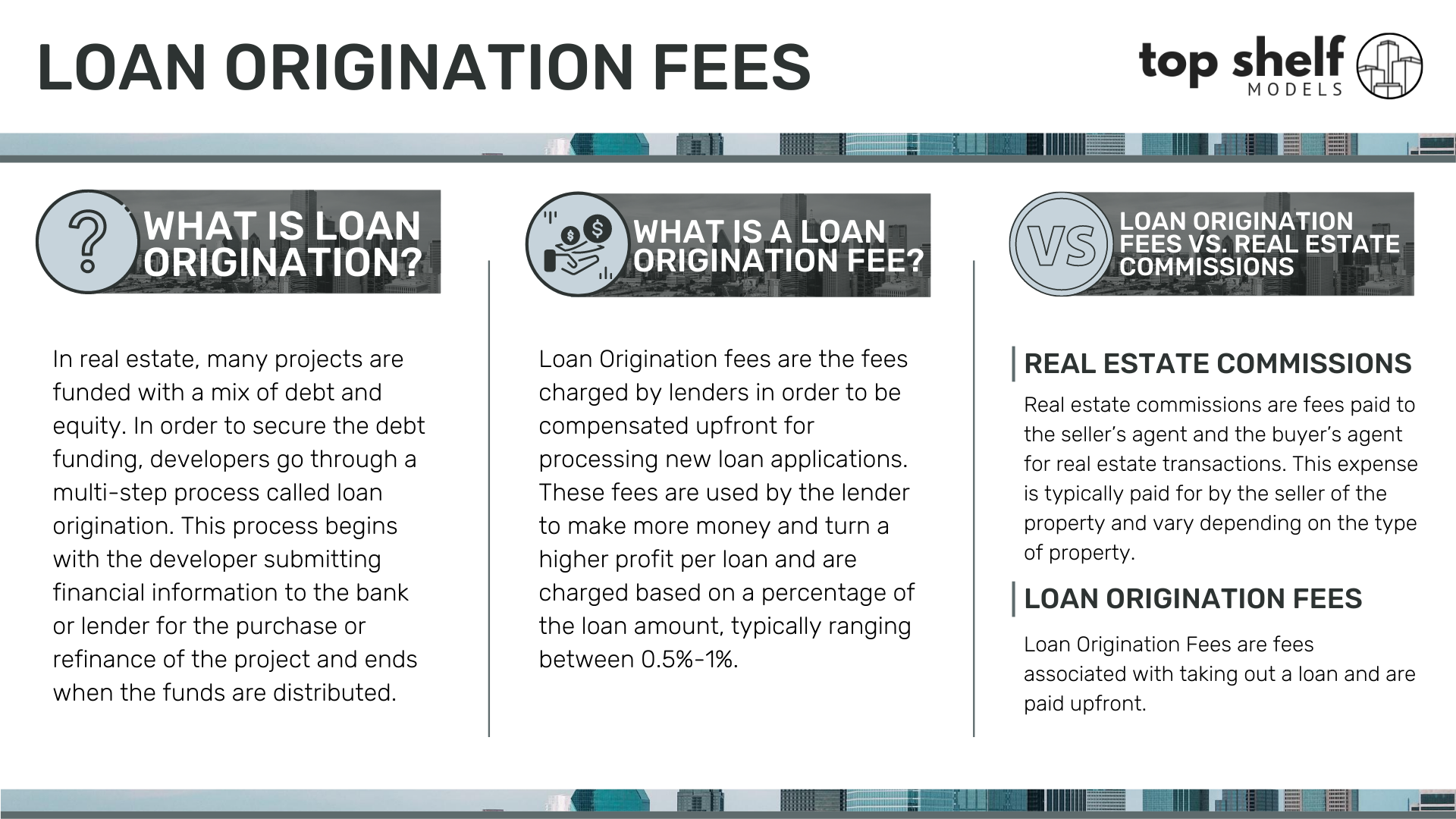

Lenders always some kind of an assessment to own a good home mortgage. Discover different kinds of appraisals. But not, for some finance, such as for instance an enthusiastic FHA Improve refi, no assessment may be required. Based on your residence and you can mortgage, a loan provider will generally need among the following the about three sizes off appraisals:

- An entire, official assessment: You pay to own a licensed appraiser in the future more and find out the house. New appraiser submits a good valuation, according to an expert investigation away from how your residence even compares to land towards you of an equivalent dimensions and you will position, considering what they ended up selling for has just.

- A drive-by the assessment: A push-by the assessment is also of the a licensed appraiser. Since title implies, the latest appraiser opinions our home in the outside, to take on their general position. A force-of the isn’t as in depth while the a full assessment. Moreover it comes to an evaluation on property value similar residential property close by.

- An automatic appraisal: An automated assessment, plus termed as a keen AVM (automatic valuation design) isnt done by a licensed appraiser. Alternatively, its created by a statistical model playing with a databases which have guidance including the purchases price of similar homes and you may assets income tax assessments. It will not involve somebody watching your property anyway.

If for example the assessment comes in below the value you would imagine your own home is worth, earliest have a look at to see that the earliest information regarding new assessment is correct (square footage, number of bedrooms, etc.). You may want to attract the financial institution to obtain the assessment examined or reconsidered.

Appraised Value and money-out

You have two main choices for delivering cash-out of your own property, a unique, cash-aside first-mortgage in the a higher harmony or the second financial, either a property Security Mortgage or a property Guarantee Distinctive line of Borrowing from the bank (HELOC). The fresh appraised value of your property is an extremely important component into the determining just how much a loan provider was ready to lend you. LTV limitations vary getting a refinance mortgage, a purchase mortgage, or good HELOC. For instance, FHA pick fund will let you acquire up to 96.5% of your own residence’s worth. However, rules for cash-aside refinancing vary. There’ll be difficulty taking a separate bucks-out first-mortgage, because of LTV limitations.

- FHA cash-out: A keen FHA dollars-aside re-finance is restricted so you’re able to an enthusiastic 85% LTV for a predetermined-speed financial.

- Traditional financing dollars-out: You are limited by 85% LTV having a fannie mae backed bucks-aside antique, fixed-rates financing on one relatives quarters that’s much of your quarters. Fannie’s allows a max 70% LTV to possess a changeable-speed mortgage (ARM). LTV limitations was lower for second house and you will resource qualities

Small suggestion

if you are looking having a profit-aside refinance mortgage, or need to refinance for the next reason, score a free of charge financial quote away from a person in the fresh new expenses home loan network.

CLTV and you may HELOC

Your capability so you’re able to refinance is additionally affected by the fresh joint loan-to-worth (CLTV). The latest CLTV lies in the entire percentage of their house’s well worth and the total count your debt of your first-mortgage as well as all other under money, second otherwise third mortgages.

Instance, a house well worth $2 hundred,000 that have a primary mortgage out of $140,000 and an effective HELOC out of $20,000, will have an effective CLTV of 80% ($160,000 from mortgages resistant to the $two hundred,000 household worth).

Any bank provided the job to own a beneficial HELOC cannot only look at the sized the brand new HELOC mortgage you prefer, however, on CLTV. A broad guideline is the fact HELOCs could be capped at an excellent 80-85% CLTV, depending on the bank as well as your compensating economic items out of loans-to-income ratio and you may possessions.

Cashing-Aside

In your particular instance, your existing mortgage harmony is actually $175,000. Four months in the past your house are respected, within the a proper appraisal, during the $220,000. When it is well worth one to now, and you are clearly restricted to 80% CLTV, maximum you might use was $176,000, and that means you wouldn’t be considered. When your financial invited your a keen LTV away from 85%, then you definitely could use $187,000. In the event that charges for the mortgage was decided when you look at the, you might almost certainly internet less than $ten,000. Of several lenders won’t offer an excellent HELOC having such smaller amounts.

The fact that you bought your house merely four month’s back would be a challenge. Considering Fannie Mae’s laws about dollars-aside refinances, «Whether your assets are ordered in early in the day 6 months, brand new borrower are ineligible to possess a funds-away deal until the loan matches the newest defer financing exception» offered for people who repaid cash towards the household and desired for taking cash-out.

Do not Pay money for an appraisal

Investing in an appraisal, at this juncture, does not apparently make feel. The common complete appraisal can cost you on the $400, although prices are very different according to the an element of the country within the hence you might be receive while the complexity of your own assessment. As an example, if you reside on the a weird assets or an incredibly pricey possessions, you will spend a top price.

Before you can purchase an assessment, I would recommend which you consult any prospective bank and acquire out of the maximum LTV to suit your possessions. It does appear odd the «robo assessment» (a keen AVM) that the financial used came back with so much lower really worth than simply the formal appraisal from less than half a-year before.

Keep in mind ahead of buying any appraisal ordered of the a great lender your appraisal have a tendency to get into the lending company, never to your, even though you purchased they. If you switch to an alternative bank, as you select a far greater price, for example, anticipate to buy another assessment.

Закладки

Comments are closed

Sorry, but you cannot leave a comment for this post.